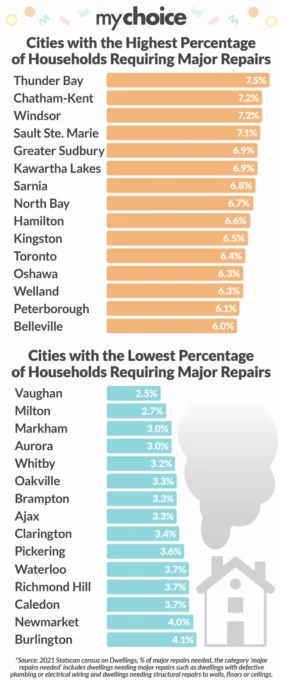

THUNDER BAY – LIVING – Does your house need major repairs? According to My Choice Insurance, 7.5% of the homes in Thunder Bay fall in this category. The disparities in home maintenance across cities in Ontario may have a bearing on home insurance rates in the province.

An internal study conducted by MyChoice, drawing from the 2021 Census data, revealed varying maintenance needs among households. Thunder Bay tops the list, with 7.5% of households reporting the need for major repairs, while Vaughan stands at the opposite end of the spectrum with only 2.5%. Major repairs encompass significant issues such as defective plumbing, electrical wiring, or structural repairs.

The financial landscape for Ontario homeowners has undergone significant changes as of December 2023, with implications for home maintenance and insurance costs. Notably, Home Equity Line of Credit (HELOC) rates have surged, surpassing 7.5%, a stark rise from the historically low rate of 2.35% recorded in 2021. This increase in HELOC rates has placed households in a challenging position when it comes to managing maintenance expenses.

The financial landscape for Ontario homeowners has undergone significant changes as of December 2023, with implications for home maintenance and insurance costs. Notably, Home Equity Line of Credit (HELOC) rates have surged, surpassing 7.5%, a stark rise from the historically low rate of 2.35% recorded in 2021. This increase in HELOC rates has placed households in a challenging position when it comes to managing maintenance expenses.

Furthermore, with the Bank of Canada showing little indication of reducing rates in the first quarter of 2024, Ontarians are cautioned about the potential for minor repairs to escalate into more significant home issues.

Regional Disparities in Home Maintenance

Aren Mirzaian, CEO of MyChoice, comments on the broader economic context: “The upsurge in HELOC rates is just one piece of the puzzle. We’re witnessing inflation in home insurance rates in Canada, with home and mortgage insurance rates increasing by 8.6% in 2023, as per the Q3 Consumer Price Index. A significant contributing factor to this rise is the inflation of building materials, leading to higher home replacement costs.”

Home Maintenance and Insurance Rates

This inflationary pressure on home insurance rates coincides with a period marked by an elevated frequency of natural disasters in Canada. These events have contributed to a surge in insurance claims and a subsequent increase in premiums. Homeowners are strongly encouraged to take measures to mitigate the risk of claims by proactively maintaining their homes to prevent minor issues from evolving into more substantial and costly repairs.

Mirzaian emphasizes the critical link between the state of home repairs and insurance costs, stating, “If interest rates remain elevated in 2024, we may witness a surge in insurance claims, potentially contributing to the upward trajectory of insurance premiums. It’s crucial for homeowners to remain vigilant about their home’s condition and ensure they have the appropriate level of insurance coverage.”